Optimising regional benefits from Council investments

For more than 30 years, the Regional Council has overseen a growing investment portfolio that had reached a gross value of more than $3 billion at 30 June 2025. This valuable asset is held by the Regional Council’s Council Controlled Organisation, Quayside Holdings Limited, on behalf of the Bay of Plenty community.

It is important that we ensure our approach to managing and structuring this asset is always fit for purpose, so that it can continue to serve and benefit the people and environment of the Bay of Plenty for generations to come.

To date, our Council Controlled Organisation (CCO) Quayside Holdings Limited (Quayside) has retained part of the income from the Port of Tauranga shareholding and the profits generated from non-Port investments.¹ Those returns have been used to diversify and grow the Regional Council’s overall investment portfolio. This is a key part of our Financial Strategy, which aims to reduce financial risk and to make sure we can respond to challenges in the future.

We are considering how the income received from these investments should be used and the most appropriate structures to hold the investments for the long term to benefit the people of the Bay of Plenty. While the structure has worked well in the past, changing demands on the portfolio may mean there are better ways to cater for the future.

The purpose of this consultation is to get community feedback on alternative ways that the investment could be held so that the Regional Council is able to make decisions about the best way forward, to maximise and secure the benefits for the Bay of Plenty of today and tomorrow.²

¹A diversified, intergenerational investment portfolio made up of private equity, real estate, listed equities and liquid financial instruments.

² Toi Moana Trust, which is invested on behalf of the Regional Council, is held separately. Change to that fund is not being considered as part of the proposed change.

What is Quayside?

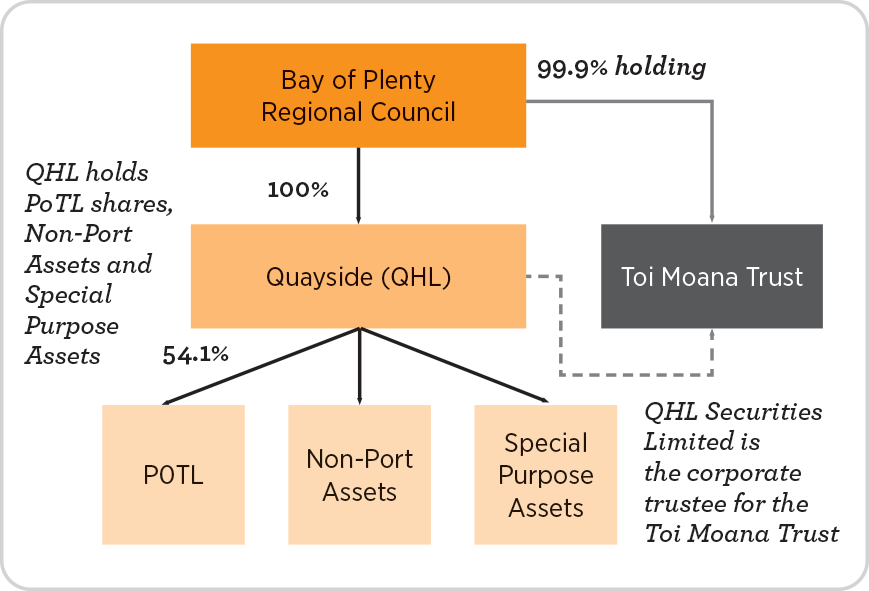

All the Regional Council’s long-term investments are currently held and managed by Quayside Holdings Limited (Quayside), a Council Controlled Organisation (CCO) that is 100% owned by the Regional Council as its investment arm.

Created by the Regional Council in 1991, Quayside’s role is to preserve and grow the net value of the total portfolio, which has a gross value of more than $3 billion.

Quayside manages the investment assets independently from the Regional Council and provides an annual dividend (payout) to the Regional Council. This is used to fund environmental projects and reduce the amount people need to pay in rates each year.

In 2024/25, this dividend was $48 million – about 23% of the Regional Council’s total income. It provided an average rates reduction of $400 per household. This meant we could provide a higher level of service on critical functions, such as biosecurity, pollution prevention and environmental improvements, with a lesser financial impact on ratepayers.

The Quayside assets are structured into three categories. Their gross values as of 30 June 2025 are:

- Port Assets (valued at $2.5b): A 54.14% Port of Tauranga shareholding*.

- Non-Port Assets (valued at $470m): A diversified, intergenerational investment portfolio made up of private equity, real estate, listed equities and liquid financial instruments.

- Special Purpose Assets (valued at $161m): This includes assets such as the Rangiuru Business Park.

These asset values will continue to change based on investment performance.

* Partial sale of shares in the Port of Tauranga would reduce the value of Port Assets and increase the value of Non‑Port Assets.

A taonga for the people of the Bay of Plenty

Taonga: A prized or treasured object.

Growing an investment portfolio worth more than $3 billion didn’t happen overnight. It’s taken more than 30 years of careful management by Regional Councillors, who were elected by our community and have been focused on what’s best for the people of the Bay of Plenty.

The fund started out with a 55% share of the Port of Tauranga valued at $53 million in 1991. Over time the fund has grown to a diversified portfolio that includes other investments. At June 2025, it had a gross asset value of $3.14 billion.

The fund is ultimately owned by the people of the Bay of Plenty.

Why do we need to think about change now?

Our investment portfolio has grown.

Its significant scale means decisions about how it is managed have far-reaching impacts for our communities, both now and in the future. It’s important that we regularly review the way we hold and manage our investments to make sure the arrangements are fit for the future.

Our region is changing and continues to grow.

The Bay of Plenty is changing rapidly. Population growth, new industries, infrastructure needs and potential local government and regulatory change are creating opportunities – and challenges – that require careful planning and investment.

It will be helpful to provide more clarity about how we can use investment returns to help meet these challenges.

The health of our environment is under strain.

Issues such as water quality, biodiversity loss and climate change demand action and funding to protect the natural resources that sustain our communities. We want to ensure that funding to support this environmental work will continue to be available for the Bay of Plenty.

The Regional Council, together with other public service providers and businesses, is facing increasing demands to respond to these opportunities and challenges.

There is pressure to invest in projects that support economic development, resilience, and community wellbeing – all while keeping costs fair and affordable.

Providing certainty in uncertain times.

Central Government has announced its intention to introduce changes that would impact regional councils and the work that they are responsible for3. While any changes will take some time to implement, we want to make decisions now that will ensure that the Regional Council’s assets remain available for long lasting regional benefit – regardless of the future shape and structure of local government in the region.

3 For more information on these proposals refer to www.dia.govt.nz/simplifying-local-government

What do we want to achieve?

We have set three purposes to define what we want to get from the investments. These purposes have then been considered as part of the assessment criteria for the proposed options.

Purpose 1: To continue using the income we get from the Regional Council’s investments to support environmental work, other Regional Council functions, and reduce rates.

We’re proposing that the amount of income allocated for this purpose is limited to $50 million plus inflation4 each year. We would ensure that dividends do not erode the capital invested so that the value of our investments at least keep up with inflation to provide continued benefit for generations to come. In 2024/25, the amount used for this purpose was $48 million. This will ensure that the Regional Council remains financially prudent as investment income increases and frees up income to support other purposes.

Purpose 2: To support development of infrastructure that delivers regional benefits, by using any surplus (extra) investment returns above the $50 million intended for Purpose 1.

This is an area that we have provided some funding for in recent years, but have contributed significantly to in the past (view a list of recent projects funded by the Regional Council). Our short-term intentions (for 2026/27 financial year only), are discussed in Topic 2: Investing in regional benefit.

Beyond this, this Long Term Plan Amendment proposes to create a dedicated revenue stream to fund projects, using surplus investment returns, that provide regional benefit and meet certain criteria. For example, this might be projects specified through a regional spatial plan. Funds for this purpose would only be available if investment returns exceeded the amount needed for Purpose 1 and the remaining value of our investments at least kept up with inflation.

Purpose 3: Ability to recycle capital.

We are currently using $200 million of debt to finance the development of Rangiuru Business Park, which is a Special Purpose Asset and an important strategic development to enable regional economic growth.

The Regional Council borrows and on‑lends to Quayside, and this debt will be repaid as the land is sold and developed. We intend to allow this debt to be drawn on to finance other projects to provide regional benefit in the future.

4 The Regional Council may receive more than this amount as a dividend from Quayside, however, the amount of this dividend that can be used for Purpose 1 would be limited.

What are we proposing?

1. Restructure our investments

To better achieve the purposes outlined above, we would need to change the way our investments are held.

Quayside has been very successful at investment management, but reviewing the structural arrangements is considered prudent considering the case for change we have outlined. It is important that we have an optimised structure in place today and the future.

With Non-Port Assets approaching $500 million (and potentially growing if the Port of Tauranga shares are divested) and a growing focus on funding infrastructure development, it is the right time to review the structure.

We’ve also looked at how other councils manage large investments, particularly the Auckland Future Fund and the New Plymouth Perpetual Investment Fund.

2. Change our Financial Strategy

To put these three purposes into effect, we need to make changes to our Financial Strategy. These changes are marked up in the proposed amendment to our Financial Strategy. This document is part of the consultation and is available for review online.

The Regional Council would have the opportunity to sense check that the funding levels for each purpose remain appropriate, by reviewing them at regular intervals that align with the fiscal planning cycles.

3. Identify options aligned to purposes

We considered a range of different ways that we could structure our investments, from holding them all together (as we do now) to splitting them into different entities to hold and manage the Port Assets, Non-Port Assets and Special Purpose Assets separately.

We concluded that the Port and Non-Port Assets should continue to be held and managed together. This is important for managing our investment risk and overall efficiency. However, the investment in Rangiuru Business Park and other future projects to support Purpose 3, could be held and managed separately or together with the other assets. This is because development projects such as Rangiuru are different to managing a commercial investment portfolio, which pays a regular dividend.

We also considered the type of entity in which the investments could be held.

Currently the form is a limited liability company, but it could be a Trust or other structure. We have outlined the options, but full details can be found in a report from PricewaterhouseCoopers (PwC)‘Optimising regional benefit’.

There’s a lot to consider

There’s growing pressure to use Quayside’s assets to fund specific projects. While these projects might bring some financial return, their greatest benefit is often for the local communities where they happen.

Expanding Quayside’s mandate in this way comes with risks. If focus shifts too much to smaller regional projects, it could weaken Quayside’s and the Regional Council’s ability to protect the value of the assets and grow the investment fund for the future.

Managing this balance isn’t simple. Every decision must weigh today’s needs against the long-term strength of the portfolio, while ensuring fairness across the region.

Quayside needs to carefully manage multiple responsibilities, for example growing investments while responding to calls for regional development, without losing sight of its core purpose and commercial objectives.

Options for consultation

We have identified three reasonably practical options:

Option 1: Status quo

Option 2: Trust model (New Council Controlled Organisation (CCO))

Option 3: Hybrid model (one or two Council Controlled Organisations (CCO)) Preferred option

Option 4: Existing community trust. This means working with an existing community trust, not yet identified. This would require further work and consideration to understand if it is practical to implement before any decisions are made. Further consultation may also be required.

We would like community feedback on which option you think will best ensure that the Regional Council’s investment purposes will be achieved over the long term.

Option 1: Status quo

Quayside (a limited liability company) continues to operate as a CCO that is wholly owned by the Regional Council, and holds and manages all of its investments through its subsidiaries. This is not a ‘do nothing’ option,

because there are opportunities to amend the governing documents of Quayside to focus on the revised investment purposes, for example altering the constitution of the company and the Regional Council’s statement of expectation.

Benefits: Ease of implementation given it’s an existing, proven structure.

Risks: The current corporate structure of Quayside could become more challenging to manage if the Regional Council wanted to support more Special Purpose Assets. Such projects provide nonfinancial benefits which are difficult to measure, complicating the accountability of a commercially focused entity. The current structure provides limited ability to ensure the longevity and security of the purposes, including ensuring their regional application, over the long term if there were significant changes to local government structures because of reform.

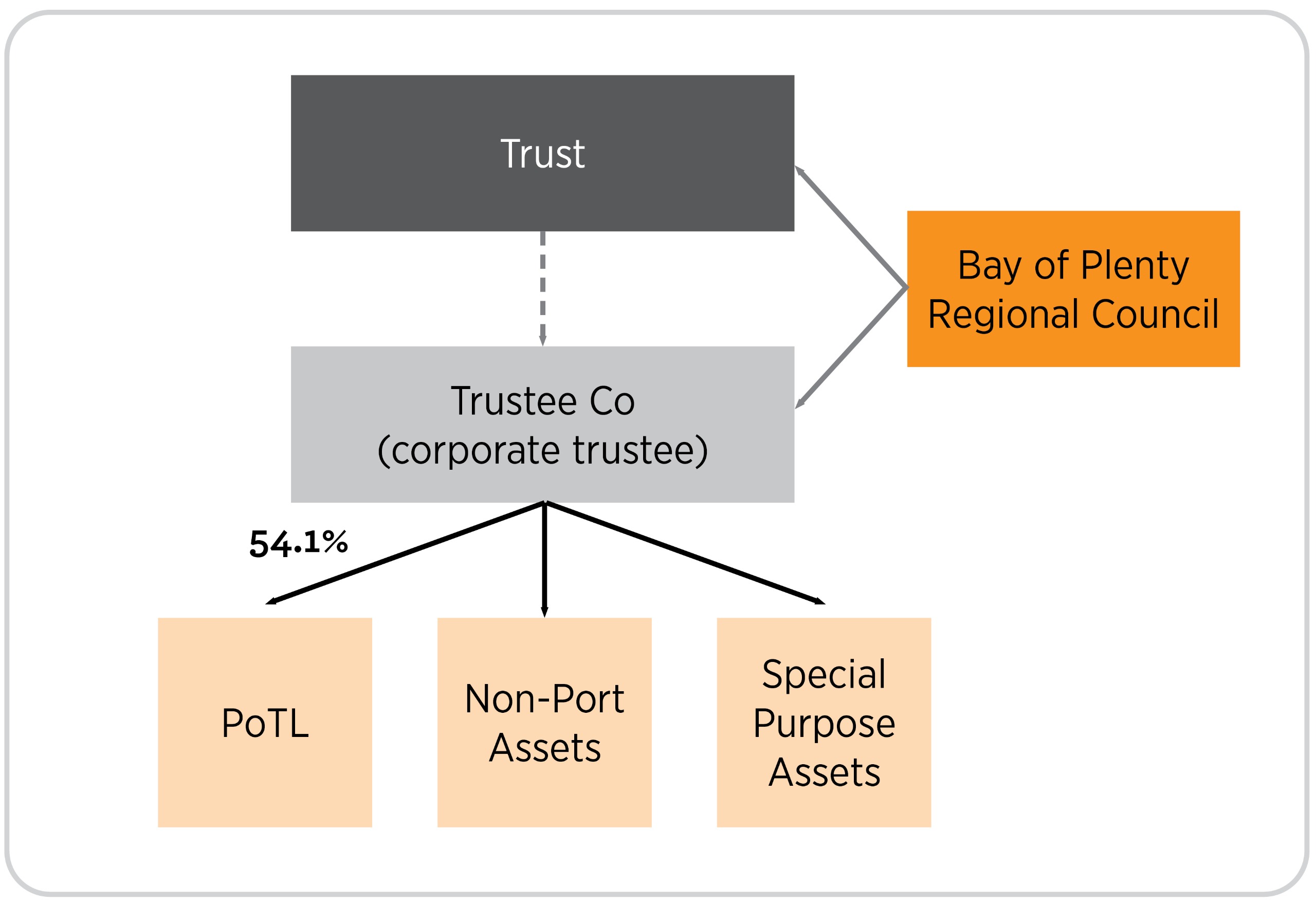

Option 2: Trust model (New CCO)

This option would involve settling a trust and transferring the investment assets currently held through Quayside and its subsidiaries into it. A corporate entity (i.e. a company) would act as trustee to hold the assets on behalf of the beneficiaries.

The final description of the beneficiaries is yet to be determined, but might be the Regional Council, any successor of the Regional Council, or other organisations within the Bay of Plenty region who advance the same purposes of the Regional Council’s investments. This would be dictated by advice as to how to effectively manage distributions. In this model, both the trust and any corporate trustee would be a CCO.5

This model would create an additional layer of separation between the Regional Council and ownership of the assets, as these would be ‘owned’ by the trust and held by the trustee. (Please refer to ‘What is a trust?’ information below).6

There are several ways this option could be implemented, including using Quayside (or one of its subsidiaries) to act as trustee, or establishing a new limited liability company (wholly owned by the Regional Council) to act as corporate trustee. We have considered whether the existing Toi Moana Trust could be used, however this is not considered practical.

If the Regional Council were to proceed with this option, it will consider the most effective implementation model, having regard for ease of implementation and cost efficiencies, management of conflicts and duties, and other considerations listed in the section Evaluating the Options, below. For example, this might mean that instead of having the Regional Council’s investments managed by the trustee, these investments could be managed by a third-party investment manager. This could also help to manage any potential conflicts of duties for the trustee.

Benefits: This model provides additional certainty by having a trustee that is obligated to act in the long-term best interests of the beneficiaries, allowing for a clearer focus on the long-term intergeneration benefits of the fund. It supports intergenerational investment and allows outsourced investment management, while still retaining strategic oversight by the Regional Council or its successor. There is a greater ability to focus on the purposes with less tension between the need to provide commercial returns and the broader outcomes sought by the Regional Council. A trust model further provides improved long-term insulation from any potential local government reform by clearly establishing long-term beneficiaries of the trust.

Risks: In establishing the trust, care would have to be taken to ensure control and accountability settings were appropriately set, any conflicts were properly managed, and tax considerations were addressed (refer to Implementation section along with Governance, management and accountability).

5 As this option might involve establishing a new council controlled organisation (CCO), the Regional Council is seeking (through this consultation process) the community’s views in accordance with section 56 of the Local Government Act 2002.

6 A decision to adopt this option may be one to which section 97 of the Local Government Act applies, because of the transfer of the shares in Port of Tauranga Limited (a “strategic asset” of Regional Council) to a new entity. Ultimately, any new entity (and therefore the shares), would still be owned by the Regional Council but via different mechanism and with greater protection for the investments. The shares held in Port of Tauranga Limited would remain a strategic asset of the Regional Council.

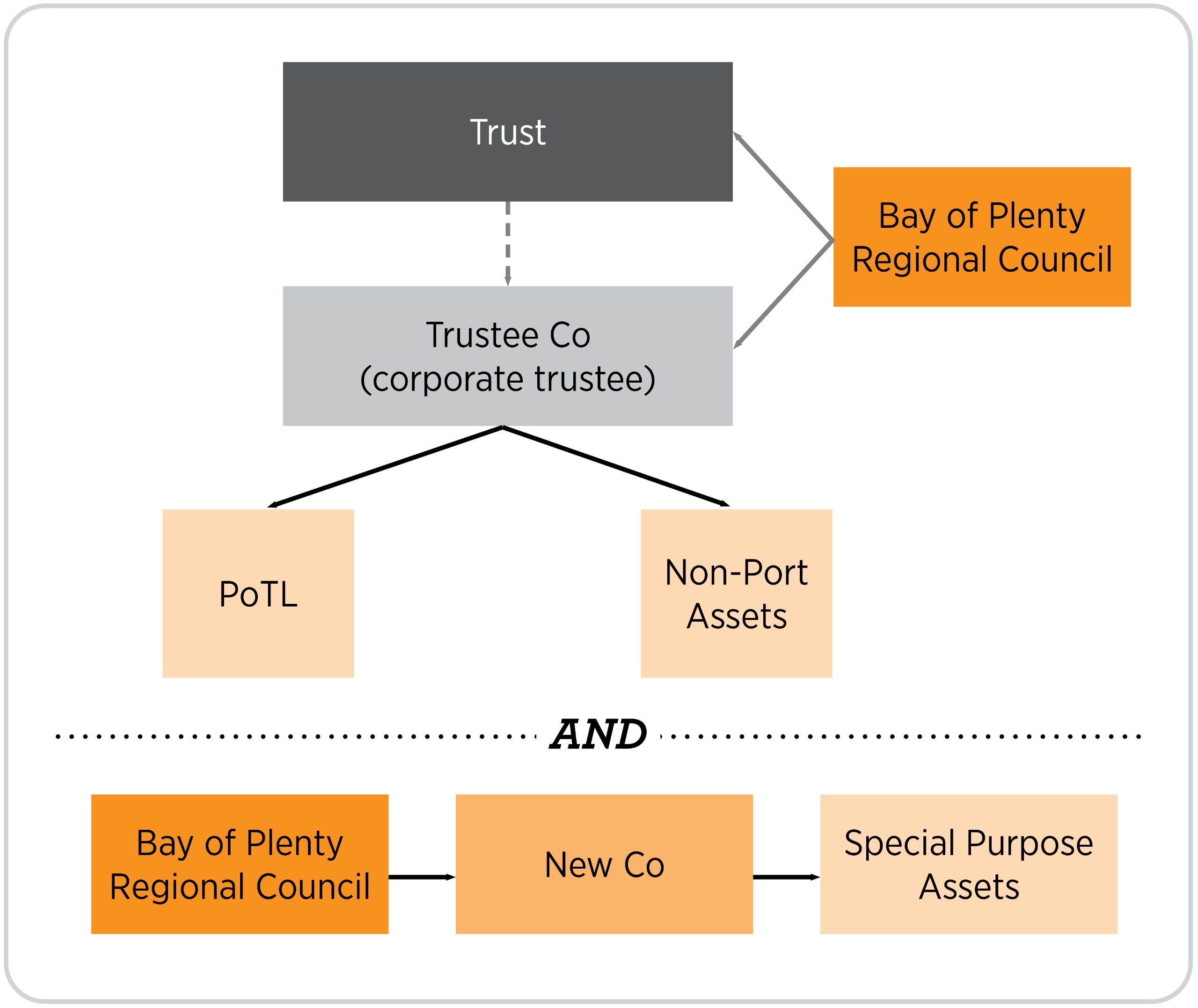

Option 3: Hybrid model (one or two new CCOs)7

Preferred option

This option would involve separating the Port and Non-Port Assets (relating to Purposes 1 and 2) from the Special Purpose Assets (relating to Purpose 3).

This model recognises that such assets have different risks and require different levels of management. Special Purpose Assets do not always provide commercial returns and are held to provide benefits to the region, for example enabling economic development or securing strategic land holdings for future infrastructure.

With this option it is likely that assets supporting Purposes 1 and 2 (together) would move to a trust model as envisaged by Option 2. Similar to Option 2, this could be implemented in several ways, including using Quayside (or one of it subsidiaries) to act as trustee, or establishing a new limited liability company (wholly owned by the Regional Council) to act as corporate trustee.

Special Purpose Assets relating to Purpose 3 could remain with Quayside (or one of it subsidiaries) or be held by the Regional Council directly or could be moved to one or more new corporate structures depending on the types of future projects being undertaken. Any new corporate entity would be a CCO wholly owned by the Regional Council, could be a limited liability company or a limited partnership, and would be subject to all of the monitoring and accountability requirements for a CCO (see below). The optimal form of the entities would depend on further advice on a case by case basis, for example tax implication.8

The Regional Council is considering this option because the assets involved in Purpose 3 (Special Purpose Assets) are different to Purposes 1 and 2 (Port and Non-Port Assets). However, if Purpose 3 assets remained separate, consideration would need to be given to its funding arrangement. The entity must have enough money upfront to finish developing its assets, so it can start generating returns and release debt capacity that can be recycled. Operational funding mechanisms for any vehicle holding the Special Purpose Assets would also need to be considered.

Benefits: For Purposes 1 and 2, this model provides similar benefits from establishing a dedicated trust as listed under Option 2. These include:

- Additional certainty by having a trustee that is obligated to act in the long-term best interests of the beneficiaries.

- Enabling a clear focus on the long-term intergeneration benefits of the fund.

- Supporting intergenerational investment and enabling outsourced investment management, while still retaining strategic oversight by the Regional Council or its successor.

- The trust model further provides improved long-term insulation from any potential local

- government reform by clearly establishing long-term beneficiaries of the trust.

By separating the Special Purpose Assets (supporting Purpose 3) and establishing bespoke structures to hold them, the governors of each entity will have a greater ability to focus on the specific purposes of the investments.

Risks: As for Option 2, in establishing the trust, care would have to be taken to ensure control and accountability settings were appropriately set, any conflicts were properly managed, and tax considerations were addressed.

7 As this option would involve establishing at least one, but possibly two, new CCOs, the Regional Council is seeking (through this consultation process) the community’s views in accordance with section 56 of the Local Government Act 2002. For clarity, as this relates to assets supporting Purpose 3 (Special Purpose Assets), this consultation only relates to potential establishment of a CCO to hold the current Special Purpose Assets being the Rangiuru Business Park Development.

8 As with Option 2, a decision to adopt this option may be one to which section 97 of the Local Government Act applies, because of the transfer of the shares in Port of Tauranga Limited (a “strategic asset” of Regional Council) to a new entity. Ultimately, any new entity (and therefore the shares), would still be owned by the Regional Council but via different mechanism and with greater protection for the investments. The shares held in Port of Tauranga Limited would remain a strategic asset of the Regional Council.

Option 4: Existing community trust

The Regional Council recognises that within the Bay of Plenty there are community trust models that already deliver significant benefits to local communities. They do this by using their investment income to provide local grants and to support community investments that have wider benefit.

One of the options the Regional Council has considered exploring further is whether it could achieve the desired purposes by partnering with an existing community trust whose values aligned and who had a proven track record of operating an intergenerational fund for community benefit.

Depending on how this option would be implemented this option could result in a significant loss of control

and influence for the Regional Council, and that would need to be weighed up against any perceived benefits of this option.

There are still a number of considerations that the Regional Council would need to work through with this option:

- Could the Regional Council guarantee the ongoing income stream which it currently uses to support environmental work rates (Purpose 1)?

- Understanding the long-term financial implications for ratepayers.

- Criteria would need to be developed to determine who the appropriate partner would be.

- The Regional Council may wish to be sure that the whole region would continue to benefit, as opposed to specific geographical areas.

- The Regional Council would wish to decide whether investments transfer, or would the Regional Council sell the investment and gift the sale funds to the chosen partner.

- CCOs have strict monitoring and reporting regimes in place to ensure appropriate accountability to the community. Appropriate accountability measures would need to be established.

We acknowledge that this option requires further investigation to understand the wider implications of this option. At this stage the Regional Council is interested in receiving feedback about whether we should do further work on this option.

Following consultation and deliberations, if this option is considered the one that best meets the purposes and criteria, further analysis and evaluation will be required in developing the specific entity arrangements. If necessary, further consultation may take place.

Other options considered

In addition to the options specified above, the Regional Council has considered other options for structuring these investments. This included the Regional Council holding these directly, but this was not considered appropriate for numerous reasons including:

- Managing these assets effectively requires specialised investment expertise and skills that are not currently held in-house.

- A level of independence in governance is appropriate given the size of the portfolio and skills required for such governance.

- Governance separation from the Port of Tauranga investment is important given the Regional Council’s regulatory function.

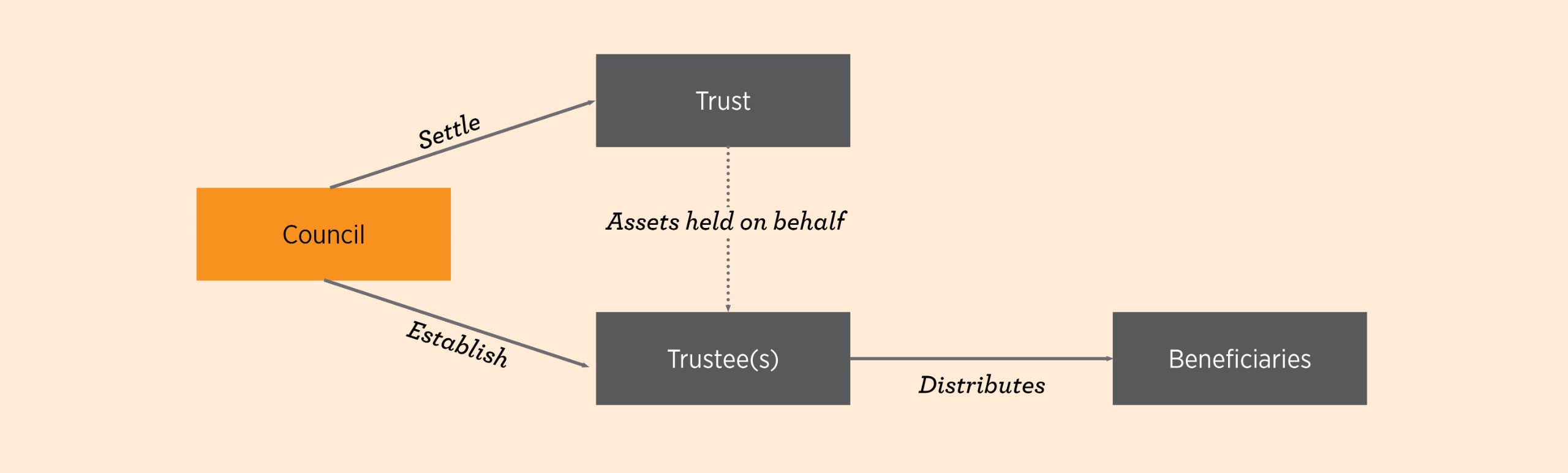

What is a trust?

A trust is a legal arrangement where a person or organisation places assets into a trust. When a trust is established, this is called ‘settling’ a trust. A trust deed is drawn up to document how the assets will be managed. The management of the assets, and decisions about the management of the assets, are made by a trustee. The beneficiaries of a trust are named in the trust deed and are the people / organisations / causes who ultimately receive any benefits from the proceeds of the trust’s assets.

A trustee has legal obligations to act in the best interests of the beneficiaries (not themselves), which is why this model is considered to have benefits.

Evaluating the options

The Regional Council developed a set of evaluation criteria for assessing the options for structures (i.e. one or more vehicles) and forms (i.e. limited liability company or trust).

The evaluation criteria used:

| Criteria | What is considered |

| Protects long-term value | Ensures that long-term financial investment remains for the benefit of current future Bay of Plenty communities regardless of sectoral / other change. |

| Enables sustainable income generation capacity | Provides the conditions for a stable, predictable income stream for community benefit, without eroding capital. |

| Enables investment for regional benefit | The structure has the flexibility and / or mandate to fund or co-fund projects that advance Bay of Plenty economic, social, environmental or cultural outcomes (not just maximise commercial return). |

| Promotes equitable regional reach of benefits | Incorporates mechanisms that help ensure all parts of the region continue to benefit from the investments (returns, distributions). |

| Provides for governance best practice | Clarity of mandate with clear roles and responsibilities and lines of accountability. Appropriate allocation of risks, transparency, and robust and efficient decision making. |

| Optimised performance and efficiency | Operating model fosters a high-performance culture and attracts the required skills and capabilities to manage the investments for the benefit of the region. Further, it optimises the group's (Quayside and Regional Council together) tax position and the operating model to minimise unnecessary cost. |

| Ease of implementation | Considers transition complexity, timing, degree of Regional Council control retained, stakeholder impact and one-off / ongoing costs required to put the option in place. |

The options noted in this consultation document represent a combination of structural and form options. These are detailed in the PricewaterhouseCoopers (PwC) report ‘Optimising regional benefit’.

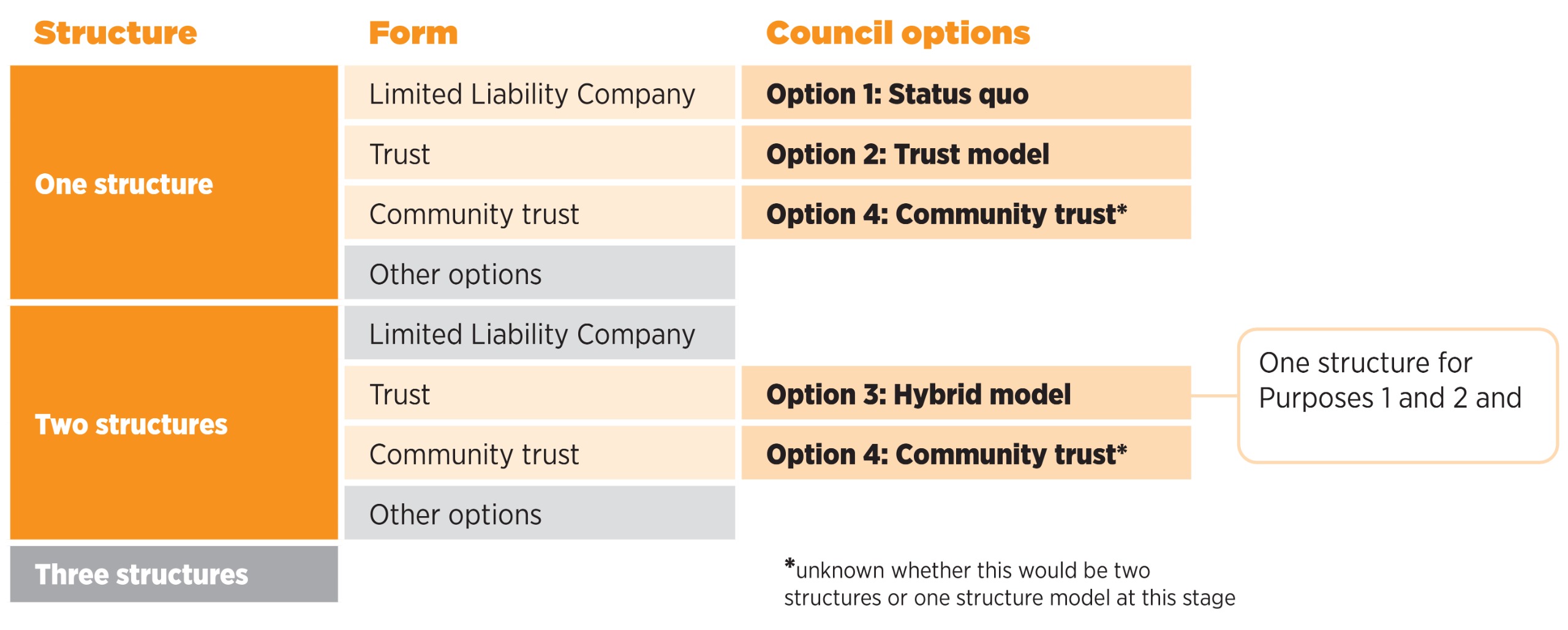

The diagram below provides a map of how the options considered in the PwC report tie to those presented in this consultation document. Greyed out boxes reflect options not progressed by the Regional Council. The form options refer to the main entity under a two-structure model.

Figure 1: How combinations of potential structures and forms have resulted in our consultation options

As illustrated in Figure 1 above, the Regional Council’s Options 1 (Status quo) and 2 (Trust option) involve using one structure to hold all the assets. Option 3 uses two structures, with the Port Assets and Non-Port Assets being in a single structure and the Special Purposes Assets held in a separate structure.

Option 4 (Community trust) could have one structure or two.

The detailed results of the structural evaluation are in Appendix 2, page 28, of the PwC report "Optimising regional benefit'.

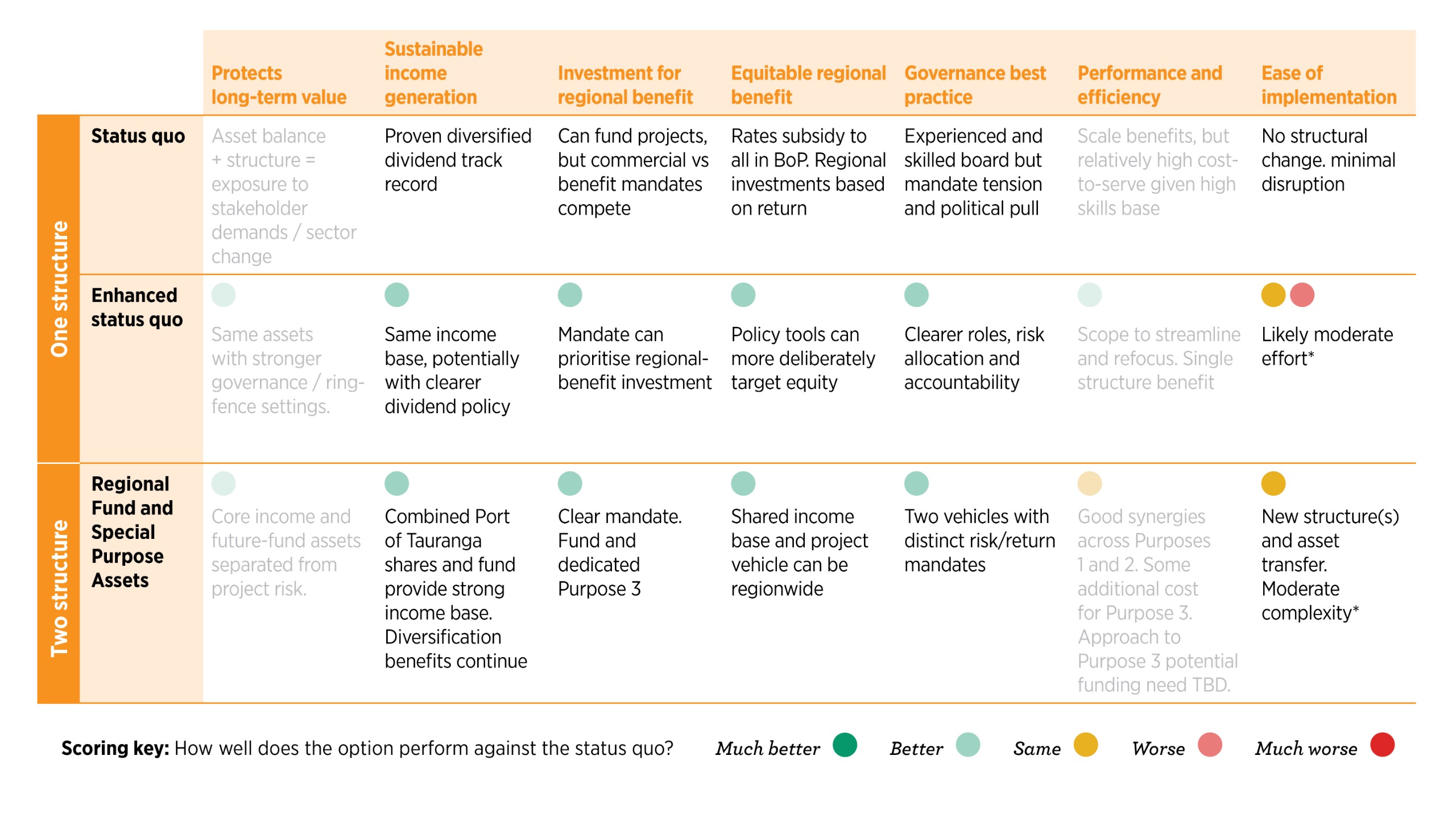

Figure 2 below is a summary of the evaluations relating to the Regional Council’s options for consultation.

Figure 2: High level structural options assessment

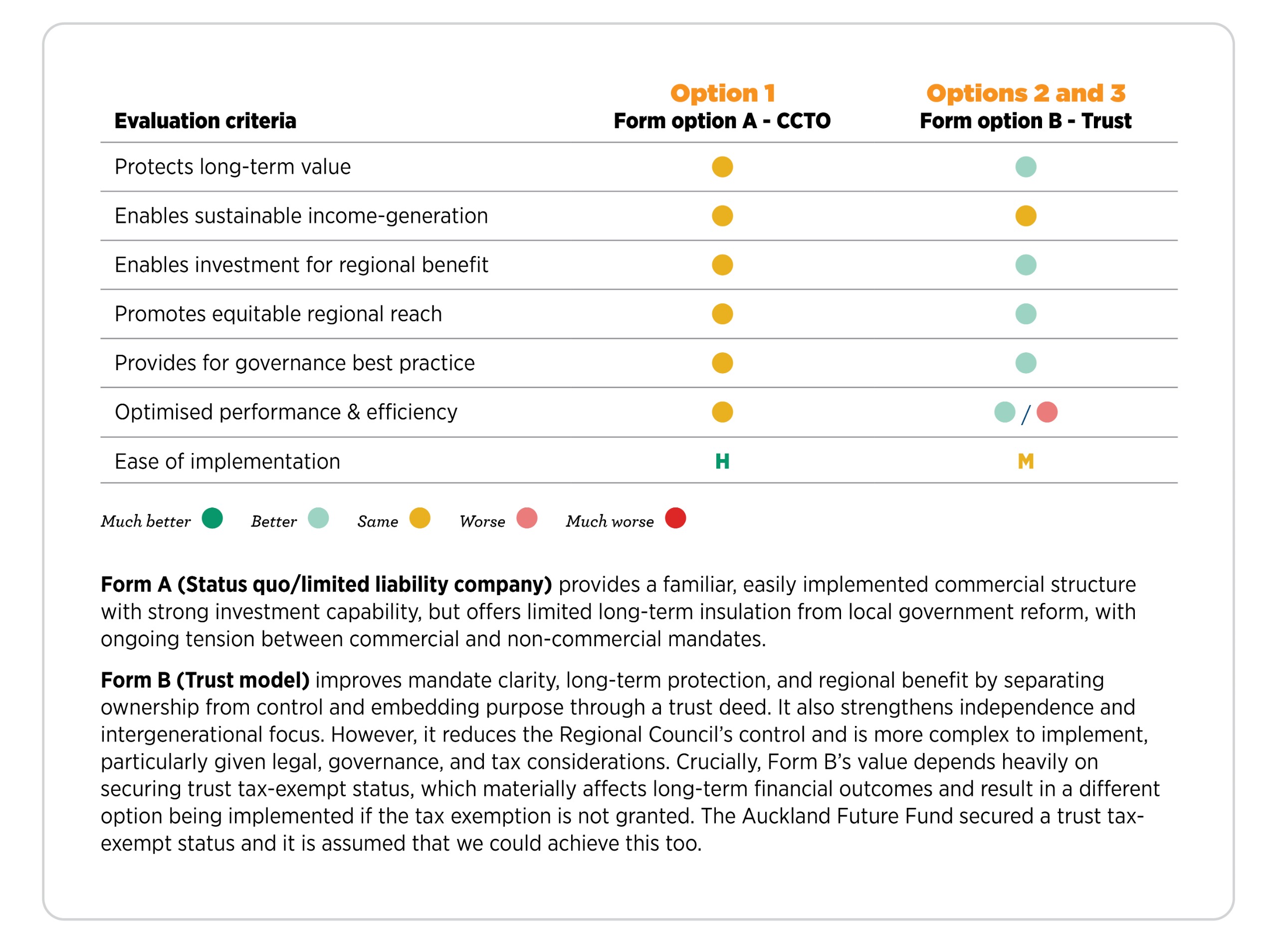

Regarding the form options, detailed evaluation against the criteria is presented on page 21 of the PwC report.

Figure 3 below summarises the evaluation of the trust form (which would be implemented with both Option 2 and Option 3), compared to the status quo (limited liability company) alongside a summary of the detailed evaluation.

The form of the Regional Council’s Option 4 (community trust) has not been evaluated because it is not possible to analyse the impacts without additional level of detail and analysis, including which community trust would be involved. This analysis would be done if we chose to progress this and carry out further work on this concept.

Figure 3: Alternatives for entity form

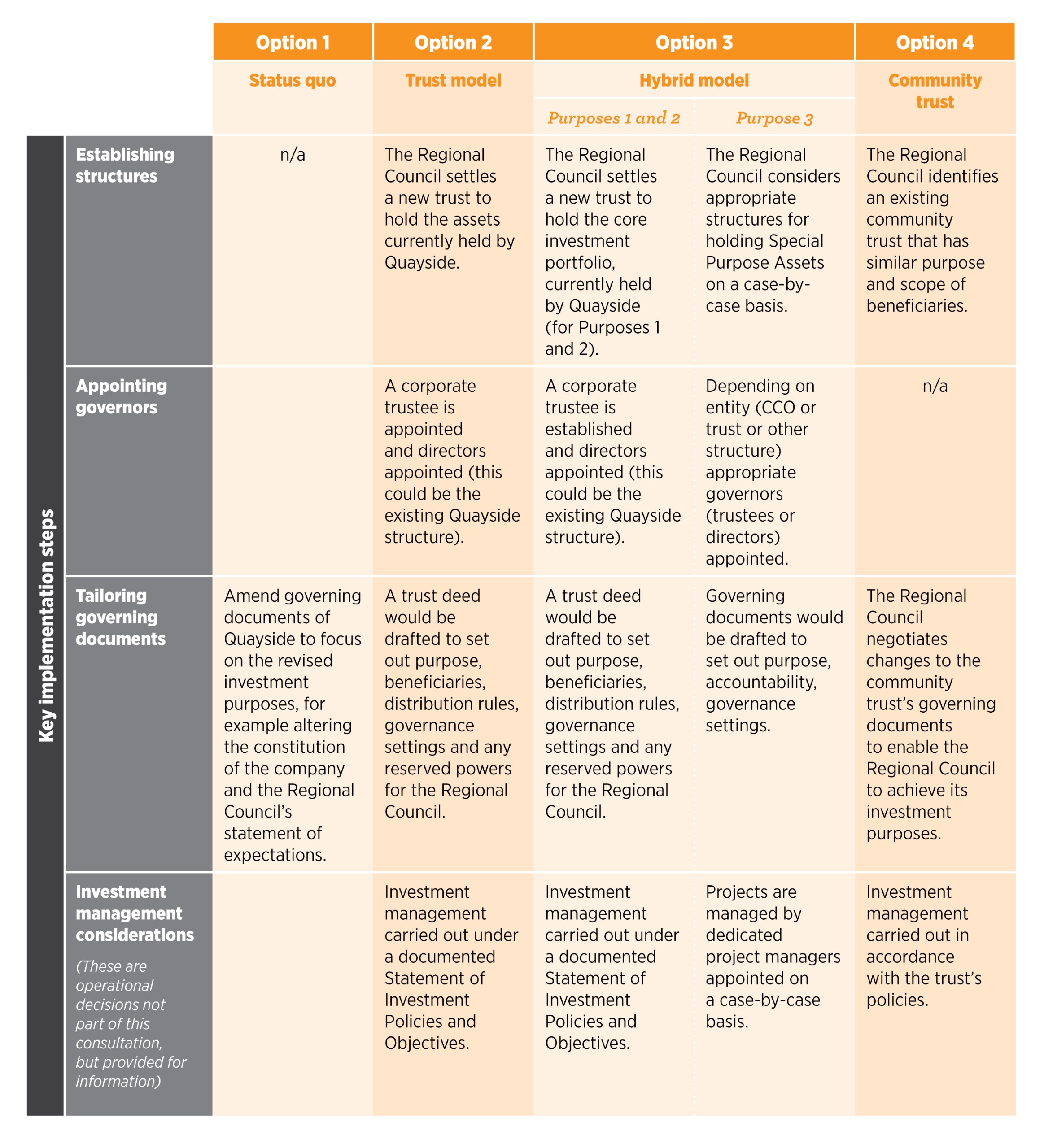

Implementing the options

If we decided to make a change to the structure of the Regional Council’s investments, this wouldn’t be immediate. Final decisions on the proposed Long Term Plan Amendment will be made in June 2026, based on community feedback on all options and advice from the Regional Council’s independent advisors on any matters raised through that feedback.

Following that, the Regional Council will be able to make operational decisions that don’t require further consultation to implement the amended Long Term Plan 2024-2034. This process would take time (up to 18 months) to ensure a smooth transition to any new structure.

Some key steps that would be involved in implementation of the options are listed below:

What else do you need to know?

Additional safeguarding

The Regional Council is also considering seeking legislative protection over the entity and / or fund, similar to what Auckland Council and New Plymouth District Council have done, to ensure that these investments are managed for long-term benefit of the Bay of Plenty region and its communities.

These councils have taken this additional step to ensure that their investment funds are safeguarded long term and are focused on benefiting not just the current, but also the future, of their communities. Taking this additional step would have the benefit of ensuring that decisions about the Regional Council’s investment funds are made independently from the Regional Council by suitably qualified managers for long-term resilience. While the Regional Council is not required to specifically consult on taking this step, for transparency we want to make these intentions clear to the community. This step would be progressed following a decision from the Regional Council on what entity (or entities) will hold its investments.

Perpetual Preference Shares

In 2008, Quayside raised $200 million through the issue of Perpetual Preference Shares (PPS) that are tradable on the NZX. The Regional Council has used the proceeds from the issue of the PPS to help fund (primarily) environmental projects.

PPS are a type of share that has no maturity date and pays a dividend to investors for as long as an organisation remains in business. While the PPS are treated as equity for accounting purposes, it is very similar to debt in that it has regular required payments to shareholders. This PPS is treated as debt for our credit rating.

Repaying the PPS could be required if Quayside reduces its Port of Tauranga Limited shareholding below 50.1%, which could happen if the Regional Council implemented the proposed new trust structures without retaining Quayside to hold the Port of Tauranga Limited shares. It is assumed that the PPS are not repaid as part of this proposal. This is because they might have already been repaid if the managed sell down of the Port of Tauranga shareholding is completed before these proposed changes are made and there are also structural options that would not require the PPS to be repaid. Quayside could be retained as either the trustee company for Options 2 or 3; or Quayside could be retained as a subsidiary of the trust for Options 2, 3 and 4. These considerations would be worked through as part of the implementation process referred to above.

If required, we would likely use borrowing from the Local Government Funding Agency Limited (LGFA) to finance the repayment. The annual payments required for the PPS and LGFA borrowing are similar or lower and there would be little net impact on overall costs if we needed to repay the PPS. The dividend payments that Quayside makes to the Perpetual Preference shareholders is not included under current purposes. If the Regional Council repaid the PPS, the payment that Quayside currently makes would be instead paid to the Regional Council to cover interest costs on borrowing from the LGFA.

Governance, management and accountability

The organisation’s governing documents (for example a trust deed or company constitution) would set out the duties of the directors and would mirror the current obligations of the Regional Council and Quayside, set out in the Regional Council’s Long Term Plan 2024-2034 and Significance and Engagement Policy. This includes the ability to divest shares in the Port of Tauranga Limited to a minimum shareholding of 28%.

Any new structure to hold investments (excluding the community trust option) would be a Council Controlled Organisation (CCO). This would enable the Regional Council to set out its expectations and require the organisation to prepare a Statement of Intent each year that sets out its objectives, activities and intentions,

and provide the basis for performance measurement and accountability. Each CCO must also provide at least half yearly reporting to the Regional Council and an Annual Report against that year’s operations. The Regional Council would require a Statement of Investment Policies and Objectives from the organisation to guide its investment decisions, and a Distribution Policy to ensure that distribution payments are sustainable. Key metrics for performance management would include investment returns compared to relevant benchmarks, compliance with investment policies, maintaining the real value of investments, and payment of distributions.

The shares in Port of Tauranga Limited are publicly traded equities, so the existing oversight and monitoring arrangements around the operations and governance of Port of Tauranga Limited will remain in place. These include rules and reporting requirements with the NZX, Commerce Commission oversight around competition law and pricing, and the Overseas Investment Office oversight for levels of foreign ownership.

We are not aware of any direct conflicts of interest arising from this proposal. Quayside will provide input as one of the Regional Council’s advisors and we are also receiving independent advice.

For any new CCO structure, we will need to determine who is responsible for governing it. The Regional Council has indicated a preference for a hybrid governance structure, one that is similar to the current governance structure of Quayside, and that includes both independent governors and elected Councillors. If this structure is chosen, we have recognised that there may be future conflicts of interest for a trustee director who is also a Councillor, given the Regional Council would be likely be a beneficiary. We currently deal with similar potential conflicts of interests where Councillors are directors on Quayside (and its subsidiaries). These are managed on a case-by-case basis depending on the nature of the decision, and in line with advice received. This ranges from Councillors declaring an interest to abstaining from voting on a matter. In any new structure this process would continue.

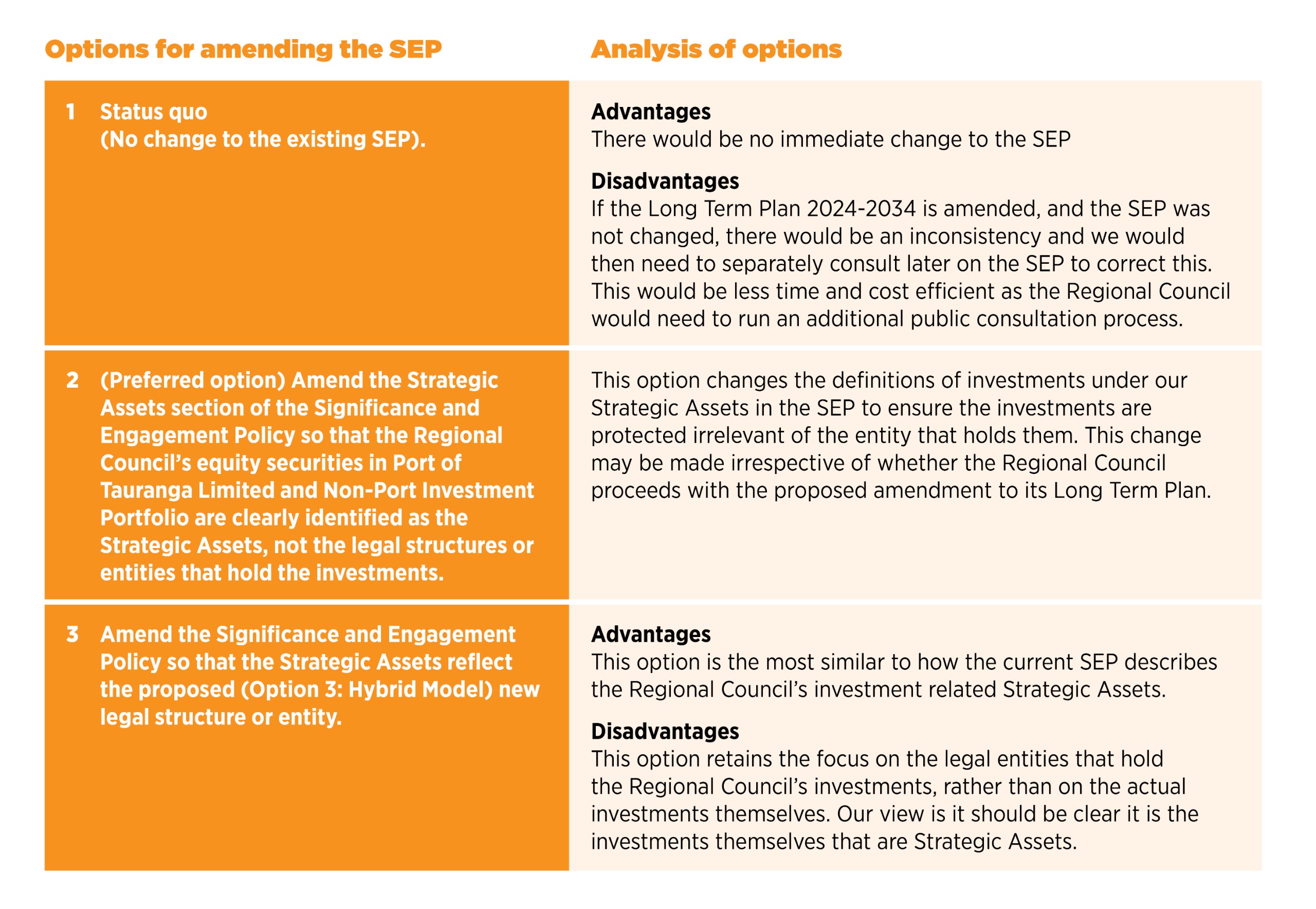

Significance and Engagement Policy

The Regional Council’s existing Significance and Engagement Policy (SEP) lists its Strategic Assets, including its shareholding in Quayside and the Regional Council’s equity securities in Port of Tauranga Limited (which is held through Quayside). We are proposing enabling changes to the definitions of Strategic Assets in our Significance and Engagement Policy to ensure the investments are protected whether they are held by Quayside or through a new legal structure.

The table below provides a summary of options the Regional Council considered for amending the Significance and Engagement Policy to align with the proposed Long Term Plan Amendment. These include Option 2, which is our preferred option. It should be noted that an amendment to the Significance and Engagement Policy may proceed irrespective of whether the Regional Council decided to proceed with the Long Term Plan Amendment.

Figure 4: Options for amending the Significance and Engagement Policy (SEP)

The Regional Council’s Significance and Engagement Policy, including the updated wording to amend the policy to reflect our preferred option (described above), is included as a supporting document online.

Q&A

Why are we consulting on this proposal?

This is a proposal to change to how we structure our investments. If implemented, it could have intergenerational impacts for the Bay of Plenty, unlocking economic growth while looking after the environment. Therefore, we need to make sure we have heard and considered all community views before making a decision on whether to implement one of the options identified as part of this proposal.

Under the Local Government Act 2002, a transfer of ownership or control of Strategic Assets to or from the Regional Council must be consulted on and provided for in the council’s Long Term Plan. The Regional Council’s 100% shareholding in Quayside and the shareholding in the Port of Tauranga Limited (noting the decision to enable a managed sell down to 28%) are Strategic Assets.

Because we are proposing to make changes to how the Regional Council’s investments are held and managed, this could result in a transfer of ownership or control of those Strategic Assets, the equity securities in particular, and requires changes to the Financial Strategy and our Significance and Engagement Policy (which is part of our Long Term Plan).

What about the proposed Port of Tauranga shareholding divestment?

The Regional Council agreed to a managed, partial sell-down of its 54% shareholding in the Port of Tauranga, to no less than 28%, as part of its Long Term Plan 2024-2034. This does not mean a decision has been made to sell, and no shares have been sold to date. Quayside may proceed with a sale when conditions permit, but there is no time frame to do so. If the Regional Council decided to make a change to the way the Port of Tauranga shares were held, this wouldn’t impact the ability of the entity holding that investment to progress with a managed, partial sell-down when conditions permitted.

What does this mean for Quayside?

A decision by the Regional Council to adopt either Options 2 or 3 will have no immediate effect other than the Regional Council’s 100% shareholding in Quayside would no longer be considered as a Strategic Asset of the Regional Council (refer to Significance and Engagement section).

Longer term it could mean that the current Quayside structure is no longer required and some or all of its structures could be wrapped up. If it was determined optimal for Quayside to remain, there would be changes to its role and mandate. For example, Quayside could be used to act as the corporate trustee of a new trust.

If this was the case, it is likely that investment management would be outsourced to manage conflicts of duties. Alternatively, Quayside could continue to provide investment management services (with a separate entity acting as trustee) or it could retain control of Special Purpose Assets such as Rangiuru (if Option 3 was adopted).

If changes were made to the Quayside structure, this also could result in a change of trustee for the Toi Moana Trust (Quayside Securities Limited currently acts as trustee). Quayside is a significant commercial business and if the Regional Council made a decision to move to either of these options, we would work closely with Quayside to manage any changes in a way that has regard for the significance of the change and those involved.

Any changes would not be immediate and a transition plan would be considered carefully and implemented. It’s worth noting that is not unusual in commercial activity of this kind to adjust operational settings to maximise efficiencies.

What about proposed Local Government reform?

Central Government has announced an intention to introduce legislation that will review the way in which local government is structured, including regional councils and the work they do9. These changes will take some time, or years, to progress. In the interim, the Regional Council remains focused on delivering value to our communities.

Work on restructuring its investment portfolio was well underway prior to the government’s announcements and will continue. However, the Regional Council will keep all interested parties – including other councils in the region – informed of its plans.

If local government changes happen in future, this proposal ensures decisions about the investments will need to be in the best interests of the people of the Bay of Plenty. Regardless of structure and governance, we think this taonga should remain for the people of the Bay of Plenty.

9 For more information on these proposals refer to www.dia.govt.nz/simplifying-local-government

Audit Statement

The Audit Statement can be viewed on pages 32 and 33 of the Annual Plan 2026/27 and Long Term Plan Amendment consultation document.

What do you think?

Question

Do you agree there is a need to restructure the Regional Council’s investment portfolio, to better achieve its objectives for its significant investment assets (which will require an amendment to the Long Term Plan 2024-2034)?

The reasons for considering change are explained in the section above headed “Why do we need to think about change now?”.

We have identified four short-listed options to restructure our investments, as described in this consultation document.

Supporting material can be found in the documents listed in the supporting documents section to the right.

Question

Which option do you prefer?

Option 1

Status quo: Quayside Holdings Limited continues to operate as a limited liability company, wholly owned by the Regional Council, and holds and manages all its investments through its subsidiaries. Potential for changes to the governing documents would be considered.

Impact on rates, debt, levels of service: None

Option 2

Trust model: Create a CCO Trust to hold all the investments currently held by Quayside Holdings Limited. Corporate Trustee would be controlled by the Regional Council.

Impact on rates, debt, levels of service: None

Option 3

Hybrid model (Preferred option): Separate the Port and Non-Port investments from the Special Purpose Assets. Create a CCO trust to hold the Port and Non-Port investments. Corporate Trustee would be controlled by the Regional Council. A different CCO entity would hold the Special Purpose Assets.

Impact on rates, debt, levels of service: None

Option 4

Existing community trust: Partner with an existing community trust with a proven track record of operating an intergenerational fund for community benefit and whose values align with the Regional Council’s.

Impact on rates, debt, levels of service: None

Note that this option requires further investigation to understand the wider implications. At this stage the Regional Council is interested in receiving feedback about whether we should do further work on this option.

Question

Do you agree to the proposed changes to the description of the strategic assets in the Significance and Engagement Policy?